is the 14th largest metro area by population in the United States with about 4.2 million people in 2010. Phoenix is the county seat of Maricopa County, and is one of the largest cities in the United States by land area.

Club West in Ahwatukee - Great Park and Great Outdoor Amenities.

Club West offers world-class golf at the prestigious Club West Golf Club. this championship course boasts 18 holes consistently ranked in the top 20 golf courses in Arizona.

"36th Best Place to Live in US by CNN in 2010"

The nation's "top places to live and learn" by GreatSchools.org. Washington-based C.Q. Press rated Gilbert the "safest municipality in Arizona, and 24th safest in the nation.

Ocotillo in Chandler - Waterfront, Golf Resort, Oasis Indoors and Out

Renowned for its resort-like communities, Ocotillo offers luxury, sophisticated and yet afforable living experience.

Val Vista Lakes in Gilbert - Water Wonderland Paradise

Val Vista Lakes offerings are the result of an artfully master planned community consisting of 900 acres. This luxury development includes twenty-four subdivisions of exquisite properties, some of which have lakefront and several of which are custom gated communities.

* Important Disclosure: The property is available at the time of this ad creation. It is very possible that an offer has been submitted or even accepted since that time. If you are interested in this property, Please call 480-721-6253 to check on its current availability.

Gorgeous 4 bedroom, 3 bath home on Ironwood, with its charming curb appeal and floor plan to match, you'll be captivated. Enter a warm and inviting living room with its hardwood flooring and custom tiled fireplace. Get ready to start cooking and making the kitchen your own! Upstairs, the master bedroom features vaulted ceilings, plant shelving, double sinks, and a private balcony that overlooks the backyard! Your new spacious backyard features a covered patio for entertaining, and the icing on the cake... a gated swimming pool

School District: 080 - Chandler Unified District

Elementary School: Shumway

Jr. High School: Willis

High School: Chandler

* Important Disclosure: The property is available at the time of this ad creation. It is very possible that an offer has been submitted or even accepted since that time. If you are interested in this property, Please call 480-721-6253 to check on its current availability.

$$ Save Thousands $$ This home on Battala is the one for you! Gorgeous 3 bedroom home in Gilbert is simply irresistible! Located in the desirable community of Power Ranch, this home has the curb appeal, character, floor plan, and neighborhood amenities that will make you Ooh & Ahh! Neutral carpet and tile throughout, along with high ceilings, make this home bright and cheery! Beautiful kitchen features cherry cabinetry, island, granite counter tops, and custom tile backsplash. Spacious living room is ideal for entertaining and leads to a low maintenance gravel backyard and covered patio! Enjoy all that this home and fantastic neighborhood have to offer, such as several community pools, fishing pond, club house, play grounds, and tennis courts! Don't miss out on this gem!

School District: 060: Higley Unified District

Elementary School: Power Ranch

Jr. High School: Power Ranch

High School: Higley

* Important Disclosure: The property is available at the time of this ad creation. It is very possible that an offer has been submitted or even accepted since that time. If you are interested in this property, Please call 480-721-6253 to check on its current availability.

First-time homebuyers have never gone through the stressful experience of buying a home, and they often learn the hard way that making a wrong turn during this process is costly and stressful. Sometimes it leads to a failed deal.

Getting approved for a mortgage, finding the right agent, searching for the perfect home and staying within a budget are some of the challenges buyers must face before they become homeowners.

Here are five common mistakes first-time homebuyers should avoid.

There's more to it than mortgage payments

Many first-time homebuyers decide to buy when they feel ready for a mortgage. But just because they can afford the mortgage payments doesn't mean they can afford to own a home, says New York attorney Rafael Castellanos, a managing director at Expert Title Insurance.

"They have an idea of what their mortgage payment is going to be, but they don't realize there's much more to it," he says.

Property insurance, taxes, homeowners association dues, maintenance, and higher electric and water bills are some of the costs first-time homebuyers tend to overlook when shopping for a place.

"Keep in mind property taxes and insurance have a tendency of going up every year," Castellanos says. "Even if you can afford it now, ask yourself if you'll be able to afford the increased costs later."

Even though it's your first home, you must think of it as a long-term commitment, says Ed Conarchy, a mortgage planner and investment adviser at Cherry Creek Mortgage in Gurnee, Ill.

"If you have to switch jobs in a year or two and may have to move for the job, you should think twice," says Conarchy. "Ideally, you should picture yourself living in that house for five to seven years."

Looking for a home first and a loan later

Homebuying doesn't begin with home searching. It begins with a mortgage prequalification -- unless you're lucky to have enough money to pay cash for your first house.

Often, first homebuyers "are afraid to get prequalified," says Steve Anderson, a broker and owner at Re/Max Benchmark Realty in Las Vegas. They fear the lender may tell them they don't qualify for a mortgage or they qualify for a loan smaller than expected. "So they pick a price range out of sky and say, 'Let's go look for a house,'" Anderson says.

And that's not how it should be done. Yes, it's more fun to go look at houses than to sit in a lender's office where you have to expose your financial situation. But that's a backward approach, Conarchy says.

"You get preapproved, and then you find a home," he says. "That way you'll make a financial decision versus an emotional decision."

Not getting professional help

New to the homebuying game? You'll need a reputable real estate agent, a good loan officer or broker, and perhaps a lawyer.

Venturing into this process alone, without professional help, is not a good idea, says Anderson. While every rule has its exception, generally, first-time buyers should not try to deal directly with the listing agent, he says.

"If you are getting divorced, are you going to go to your husband's attorney for help? Of course not," he says. "Same here. If you go to a listing agent, they are only going to show you their listings. You must find a buyers' agent to help you."

If you hire an agent without a referral from friends or family, ask the agent to provide references from previous buyers. The same goes for loan officers or mortgage brokers.

"It's very hard for first-time homebuyers because they don't know who they are dealing with," Anderson says.

It's crucial to find a professional who will give you "truly independent advice," Conarchy says.

Sometimes that means hiring a lawyer, says Castellanos.

"You are about to make what is possibly the largest single investment of your lifetime," Castellanos says. "You want to make sure it's done right."

Exhausting entire savings on the down payment

Spending all or most of their savings on down payment and closing costs is one of the biggest mistakes first-time homebuyers make, Conarchy says.

"Some people scrape all their money together to make the 20 percent down payment so they don't have to pay for mortgage insurance, but they are picking the wrong poison because they are left with no savings at all," he says.

Homebuyers who put 20 percent or more down don't have to pay for mortgage insurance when getting a conventional mortgage. That's usually translated into substantial savings on the monthly mortgage payment. But it's not worth the risk of living on the edge, says Conarchy.

"I'd take paying for mortgage insurance any day over not having money for rainy days," he says. "Everyone -- especially homeowners -- needs to have a rainy-day fund."

No furniture shopping until the deal is closed

You have prequalified for a loan. You found the house you wanted. The contract is signed and the closing is in 30 days. Don't celebrate by buying furniture or a car, if you plan to finance those purchases.

In this tight lending environment, lenders pull credit reports before the closing to make sure the borrower's financial situation has not changed since the loan was approved. Any new loans on your credit report can jeopardize the closing.

Buyers, especially first-timers, often learn this lesson the hard way.

"They sign the contract and they want to go buy new furniture for the house or a new car," Anderson says. "I remember one case where just before closing, the buyer drove to the office and said, 'Look at my brand-new car.' I told them, 'You better go back to that dealership.'"

Luckily, the dealership agreed to wait a couple of days to report the loan to the credit bureaus, he says. Otherwise, it could have killed the deal.

The National Association of REALTORS® is predicting existing-home sales will jump 7 to 10 percent in 2012 to the highest level in five years, based on an "uneven but higher sales pattern" so far this year.

Pending home sales fell a seasonally adjusted 0.5 percent from January to February, which was up 9.2 percent from the same time a year ago, NAR said today in releasing its latest Pending Home Sales Index.

Last week, NAR reported a similar trend for existing-home sales, which were down 0.9 percent from January to February, but up 8.8 percent from a year ago.

The pending sales data released today provides a glimpse into more recent trends, because it tracks homes that were under contract in February -- deals that will in most cases be finalized within one or two months.

NAR said 31 percent of REALTORS® experienced contract failures in February, in some cases because buyers' mortgage applications were rejected or because appraisals came in below the negotiated price.

In the Northeast, NAR's index slipped a seasonally adjusted 0.6 percent from January but was up 18.4 percent from a year ago.

The Midwest saw a month-over-month gain of 6.5 percent and a 19 percent gain from a year ago.

Pending home sales fell 3 percent in the South from January to February, but were up 7.8 percent from a year ago.

In the West, the index declined 2.6 percent from January to February and was 1.8 percent below the index rating in February 2011.

In its latest economic forecast, NAR predicts existing-home sales will total 4.65 million in 2012, up 9.1 percent from last year. That forecast assumes that the U.S. economy will grow at a 2.3 percent annual rate and add 2.7 million jobs this year.

Go GREEN without mowing! Healthy fun in heart of Power Ranch on cul de sac, very near famous lake & club house, ymca, olympic pool, fishing, high style 2012 makeover; single level split plan, 4 bedrooms 2 baths, 2 car gar, rv gate, big & deep backyard with pebble textured pool with fancy lights, storage shed, covered patio with extra paved areas, neat & low maint yard, formal dining & living room, high ceilings, newly upgraded entertainer's kitchen with new granite slab counters & bar, new crown & trim, new faucet & sinks, new hardware, all new stainless appliances, master suite has pool views, double vanity, sep soak tub & shower, long closet, new lighting, tile, new paint, new carpet, fans, neutral colors, quiet area, ideal friendly street atmosphere. NOT Short Sale, NOT Bank Owned. NO WAITING!

* Important Disclosure: This property is listed by Jeanne Welnick under Keller Williams Realty Sonoran Living. The property is available at the time of this ad creation. It is very possible that an offer has been submitted or even accepted since that time. If you are interested in this property, Please call 480-721-6253 to check on its current availability.

One of the biggest myths in the real estate industry is that it is cheaper to rent than to buy. In 71 percent of the cities in the U.S., owning is now currently cheaper than renting.

In 2011, 1.4 million new households entered the rental market due to foreclosures and demographics -- i.e., the 80 million members of Gen Y are at their prime time for starting new careers, getting married and having kids. At the same time, the number of new homes being built has dropped substantially. As a result, the demand for rental properties has skyrocketed.

Many experts are predicting that rent increases will run as high as 5 to 10 percent per year over the next five years.

What can you do to help persuade today's renters to become buyers? Here are some suggestions:

1. Real estate keeps pace with or exceeds the rate of inflation

Everyone today is concerned about the level of federal spending. A key concern is inflation. Hard assets -- real estate, gold and silver, among them -- have historically served as hedges against inflation. In fact, even in the areas hit hard by foreclosures, virtually all of them have shown substantial increases in real estate values when viewed in the long term.

To illustrate this point, when my father died in 1998, his house in California was valued at $168,000. At its peak in 2006, his house was worth almost $600,000. Today it's still worth about $350,000. That's still a 108 percent gain in value in 13 years. While not every area has seen such increases, more than 90 percent of all homes are still worth substantially more than they were 10 years ago.

To market using this concept, here's the headline to use on your postcards or other print advertising: "What's the best hedge against inflation? Real estate: the only hedge against inflation that you can live in."

2. The lowest interest rates since the 1950s

A major reason that buyers should purchase now is that interest rates are close to all-time lows. When I started in the real estate business in 1978, interest rates were 9.75 percent and soon hit 10 percent. In the downturn in the 1980s, they jumped as high as 21 percent. In the early 1990s, they were at 12 percent.

If your buyers are waiting because they think prices may drop more, this is a poor idea. Here's why: With the government running huge deficits, it will have to sell Treasury bills to cover the debt. Investors are feeling skittish about purchasing these securities.

This means the government will have to increase the rate of return in order to get more investors to purchase. When the government increases these rates, the cost of home mortgages will increase along with them.

3. Increasing interest rates add up fast

An interest increase of 1 percent results in about a 25 percent increase in interest costs over the life of a 30-year fixed-rate loan. An increase of two percentage points in interest results in a whopping 50 percent increase in the amount of interest paid. That's why it's smart to buy now when rates are at historic lows.

4. The market may have already bottomed

When buyers say they're afraid the market hasn't bottomed yet, take a look at your local market in their specific price range. Look at the number of months of inventory now vs. six months ago and one year ago.

If the number of months of inventory is declining, that lets you know that you may have already reached the bottom of the market. On the other hand, if the number of months of inventory is still increasing, then there's a good chance you haven't hit bottom yet.

To drive this point home, ask buyers how much further they believe the market will drop as a percentage. Most will give you an answer under 10 percent. Then point out that if they have to pay an extra percentage point in their interest rate it will cost them 25 percent more in interest over the life of a 30-year loan. Buying now, assuming that they keep the property, saves them 15 percent of their loan amount, even if the market declines by 10 percent.

5. Build your wealth, not your landlord's

There are two other reasons why it can be smarter to purchase than to rent. When you purchase, you lock in a payment at today's interest rate.

Assuming that there is inflation at the average rate of 2.54 percent per year (the U.S. average), 10 years from now your monthly payment will be the equivalent of 75 cents on the dollar.

In other words, a $2,000 payment 10 years from now would be the equivalent of $1,500 in today's dollars. In 20 years, it would be the equivalent of $1,000 in today's dollars.

In contrast, renters may continue to receive rent increases. An additional benefit of homeownership: each month you pay your mortgage, you accumulate equity. In contrast, renters are paying down their landlord's mortgage, allowing the landlord to accumulate the wealth rather than them. Thus, in the long term, for some individuals it's almost always smarter to buy rather than rent.

If you're considering buying a home, securing a mortgage loan is a key part of the process. However, you’re probably wondering: how do I find the best mortgage loan for my financial needs? Generally speaking, there are two types of mortgage loans:

A fixed-rate mortgage offers a rate that stays the same over the life of the loan. This type of loan generally has a longer term and may be good if you plan to own your home for a long time.

An adjustable-rate mortgage offers an interest rate that adjusts based on market conditions (it goes higher or lower) after a specified time period. This type of loan may be good for people who need an initial lower monthly payment.

Consider the following factors to help you gain insight into the kind of home you can afford, and the type of mortgage that will best fit your financial situation:

How long do you plan to own the home?

Some loans have longer terms (from 15 to 40 years) that typically work well when you plan to stay in the home for a long time. Other loans have lower interest rates for a shorter term, and may be attractive if you plan to move in five to seven years.

CONSIDER: How many years do you plan to stay in the home? Will you move within seven years, or is this the place to "settle down?"

How much can you afford as a down payment?

20% of the cost of the home is standard for the down payment on a conventional loan, but there are loans that allow you to put down as little as 5 or 10%.

The higher your down payment, the lower your monthly mortgage payment will be.

CONSIDER: How much can you realistically afford as the down payment?

What is the general price range for other homes in your neighborhood?

How many homes are for sale in the area? How are they priced? Do you have a list of comparable properties?

Are there other neighborhoods that catch your eye? How are the homes in these other areas priced?

CONSIDER: Which area/home features the best combination of location, quality, and cost for you.

Which of the following is more important to you?

To have low monthly payments?

To pay less over the life of the loan, even if monthly payments are high?

Some loans offer lower monthly mortgage payments over a long period of time. Other loans are designed to be paid in a shorter time frame, but have higher monthly payments.

CONSIDER: Which situation would work best for you? It helps to be clear about your financial goals and resources.

Your credit history

Mortgage lenders will look at your credit history and credit score to determine your track record for paying off debt.

CONSIDER: Do you have a good credit score? Review your credit report to find out.

Corner lot HUD home in Kyrene School District! Enjoy a spacious floor plan with vaulted ceilings, custom paint, and neutral carpet/tile throughout! Living room is large and features a built in entertainment niche, so get ready to entertain! Cozy kitchen features all white appliances and is ready for you to whip up some great home cooked meals. If you're into privacy and relaxation, fall in love with the master bedroom, which also features its' own private sliding door to the backyard! Out back you will find a covered patio and plenty of free reign to landscape to your liking! Come enjoy this lovely Chandler home today!

* Important Disclosure: The property is available at the time of this ad creation. It is very possible that an offer has been submitted or even accepted since that time. If you are interested in this property, Please call 480-721-6253 to check on its current availability.

Great cul-de- sac HUD home complete with 4 bedrooms, 2 baths, vaulted ceilings, and a wonderful floor plan! This home is awaiting your family's loving touch! Enjoy a spacious living room that leads to a quaint kitchen with eat-in dining area. A few of those ideas you've cut out of home and garden magazines will finally come in handy in making this home your very own! Enjoy a cozy master bedroom that offers the privacy that you deserve! The backyard offers low maintenance landscaping, which you could very well turn into your own backyard getaway! Enjoy a covered patio for entertaining and throwing barbecues in the summer.

* Important Disclosure: The property is available at the time of this ad creation. It is very possible that an offer has been submitted or even accepted since that time. If you are interested in this property, Please call 480-721-6253 to check on its current availability.

Last week brought bad news for wealthy unmarried couples who own homes together. The U.S. Tax Court held that the $1.1 million limit on the mortgage interest deduction must be applied per residence, not per taxpayer, even where the co-owners are unmarried and file separate tax returns.

Home mortgage interest for a loan or loans totaling $1 million is deductible as an itemized deduction. Interest on a home equity loan -- for a primary or second home -- of up to $100,000 is also deductible. Thus, you can deduct the interest on a total of $1.1 million in home loans each year. If you borrow more than that, the additional interest is not deductible.

If a married couple own a home or homes and file a joint return, the $1.1 million limit applies to them both together. If they file separately, the limit is cut in half for each. So, either way, married couples are limited to deducting the interest on only $1.1 million.

But what about when unmarried couples purchase homes together and file separate returns -- does the limit apply to them both together or to each separately?

Charles and Bruce, an unmarried couple, purchased a principal residence in Beverly Hills, Calif., and a second home in Rancho Mirage, Calif., as joint tenants. They each filed separate tax returns. Their total mortgage debt was more than $2.7 million.

Charles and Bruce each deducted on their separate returns the interest on $1.1 million of their loans. Thus, together they deducted the interest on $2.2 million.

The Internal Revenue Service said that Charles and Bruce together could deduct only the interest on $1.1 million. The couple argued that because they were not married, the limitations on married taxpayers don't apply to them.

Instead, they claimed that when unmarried people co-own a house the $1.1 million limit applies to each individual taxpayer.

The Tax Court sided with the IRS. It held that the $1.1 million limit applies per residence, not per taxpayer, even where a home is co-owned by unmarried taxpayers.

Thus, even though they were unmarried and filed separate returns, Charles and Bruce could together deduct the interest on only $1.1 million of their mortgage debt.

Instead of deducting more than $76,000 in mortgage interest on their individual returns, they could each deduct only $38,000.

Unmarried people who purchase expensive homes should keep this limitation in mind.

Traditional sale! 5 Bedrooms, 5 Bathrooms, 4114 sq/ft in Ahwatukee. Come home to the luxury of the Sanctuary. Beautiful custom home w NO NEIGHBORS BEHIND. This single level has it all. 12'coffered ceilings, travertine flooring, Roman columns, Gourmet kitchen w/granite countertops, Elegant master bedroom w/dual shower, Jacuzzi tub, 2 way fireplace to bath and sitting room. Large master closet includes a separate cedar closet. Four bedrooms boast their own full baths. Fifth bedroom is used as a study/library. Full bath leading into the house off the pool area, plantation shutters and windows galore to enjoy exclusive mountain and lake views. Shown by appointment only.

* Important Disclosure: This property is listed by Donna Leeds under Keller Williams Realty Sonoran Living. The property is available at the time of this ad creation. It is very possible that an offer has been submitted or even accepted since that time. If you are interested in this property, Please call 480-721-6253 to check on its current availability.

Welcome to the Lakewood homes and real estate portal: your single stop for finding a home in Lakewood. Here you can search every available home for sale in Lakewood.

As of today there are many homes and properties for sale that are available to search. The number of homes changes daily, so be sure to keep coming back right here, to the best site for Lakewood homes for sale.

Buying a home is a trying and complicated process. It often strains relationships and puts an enormous amount of stress on buyers physically, mentally and financially. That's why the folks at the Boston Globe have put together this list of 10 things to keep in mind as you weather the home-buying storm.

1. Get your financing in order

"The seller wants to know that if they do accept the offer, that barring catastrophic title issues or inspection issues, the deal is going to go through," said Gary Dwyer, broker-owner of Buyer Agents of Boston. Another expert recommends having a full pre-approval within the past 30 days: "Six months is no good anymore, because the rules keep changing."

2. Understand your time horizon

"As a shorter-term buyer, you might consider whether the place is a good investment, and if it's the kind of property that's going to be attractive for the next buyer...A house near train tracks, for instance, is probably not what most people are looking for. But for someone who's planning to stay longer, a good school system or larger lot size might make up for the trains thundering past."

3. Know the overall market conditions

Investigate what comparable properties have sold for over the past three to six months, Dwyer advises. If you're not working with an agent, sites with pricing information such Zillow.com or Trulia.com could help.

4. Search and buy within your means

"If the housing crisis has taught us anything, it's that buying with the expectation that prices will continuously go up — and that if you can eke out the payments each month, you'll be in a good spot in the long run — isn't such a good idea."

5. If you're waiting for prices to go lower, think again

Real estate is a bit like the stock market, Hillman says, in that it's unpredictable. Though some people might be waiting on the sidelines for housing prices to dip lower, she says, "looking at the numbers, I can't see them continuing to go down."

6. Don't get too sucked in by appearances

Buyers should keep in mind that many sellers will try to present their homes in the best possible light. "If the house has been staged, what [potential buyers] forget is that all that stuff is going out when [the sellers] leave," says Needham realtor Harriet Lieb. "Sometimes you're better off buying something that needs a little decorating, because it's going to take on your own look anyway."

7. Have questions prepared

"Sellers and their agents should be prepared to answer questions including how old the roof, heating system, hot water heater, and windows are; if the basement has taken water in the time the seller has been there, and if there's a sump pump; and what utilities and homeowner insurance generally cost... If there's been recent renovation work, buyers should find out of all building permits have been signed off and if all of the contractors and sub-contractors have been paid in full. If there's a pool, buyers should ask if the seller has a permit from the city or town."

8. If you're thinking of buying a brand new house...

Consider that a home that's been lived in has been tested, says Lieb. The seller will be able to tell you if the basement takes on water in a rainstorm, for instance.

"People will pay a lot of money for a brand new house. I tell people, it's only new once. It's like a car — you drive it out of the lot, it's not new," she says.

9. If you're buying a condo, know the rules

"Condo lending rules have become more stringent, making it difficult for some would-be buyers to get financing. Lenders generally want buildings to be at least 50 percent owner-occupied, Dwyer says."

10. Think about a home's intrinsic value

"[Buying a home] has always been a consumption decision and an investment decision," says Nicolas Retsinas, director of the Joint Center for Housing Studies at Harvard. In recent years, "we moved that dot along the continuum, and it became an investment decision... Questions such as 'Is this where I want to raise a family' and 'Is this close to the things that are important to me' will factor more into the decision."

Traditional sale! Stunning ''Del Mar'' floorplan. Former model home located in prestigious gated Diamond Ridge II community. Lot size is over 10,000 sq ft. The minute you walk through the front door you will feel the warmth of this classic Knoell home. It is meticulous from top to bottom. Fifth bedroom is used as a study, has no closet. Spacious master bedroom with sitting room along with separate entry. Beautiful upgraded kitchen and new porcelin flooring throughout,butlers pantry, wetbar, double oven and large walk in pantry.

Family room with fireplace.Plantation shutters throughout.Three bedrooms have new wood flooring. Three full baths.

* Important Disclosure: This property is listed by Donna Leeds under Keller Williams Realty Sonoran Living. The property is available at the time of this ad creation. It is very possible that an offer has been submitted or even accepted since that time. If you are interested in this property, Please call 480-721-6253 to check on its current availability.

Over the past several years, millions of homeowners have had billions of dollars in mortgage debt forgiven, either through foreclosure, refinancing or short sales. It's important for real estate professionals and homeowners to understand that mortgage debt forgiveness has significant tax consequences.

Here are 10 things the Internal Revenue Service says you should know about mortgage debt forgiveness:

Normally, when a lender forgives a debt -- that is, relieves the borrower from having to pay it back -- the amount of the debt is taxable income to the borrower. Thus, a homeowner who had $100,000 in mortgage debt forgiven through a short sale would have to pay income tax on that $100,000, as an example. Fortunately, under the Mortgage Forgiveness Debt Relief Act of 2007, you may be able to exclude from your taxable income up to $2 million of debt forgiven on your principal residence from 2007 through 2012. This means you don't have to pay income tax on the forgiven debt.

The limit is $1 million for a married person filing a separate return.

You may exclude from your taxable income debt reduced through mortgage restructuring, as well as mortgage debt forgiven in a foreclosure.

To qualify, the debt must have been used to buy, build or substantially improve your principal residence and be secured by that residence.

The Mortgage Forgiveness Debt Relief Act applies to home improvement mortgages you take out to substantially improve your principal residence -- that is, they also qualify for the exclusion.

Second or third mortgages you used for purposes other than home improvement -- for example, to pay off credit card debt -- do not qualify for the exclusion.

If you qualify, claim the special exclusion by filling out Form 982: Reduction of Tax Attributes Due to Discharge of Indebtedness , and attach it to your federal income tax return for the tax year in which the debt was forgiven.

Debt forgiven on second homes, rental property, business property, credit cards or car loans does not qualify for the tax-relief provision. In some cases, however, other tax-relief provisions -- such as bankruptcy -- may be applicable. IRS Form 982 provides more details about these provisions.

If your debt is reduced or eliminated, you normally will receive a year-end statement, Form 1099-C: Cancellation of Debt, from your lender. By law, this form must show the amount of debt forgiven and the fair market value of any property foreclosed.

Examine the Form 1099-C carefully. Notify the lender immediately if any of the information shown is incorrect. You should pay particular attention to the amount of debt forgiven in Box 2 as well as the value listed for your home in Box 7.

The IRS has created a highly useful Interactive Tax Assistant on its website that you can use to determine if your canceled debt is taxable. The tax assistant tool takes you through a series of questions and provides you with responses to tax law questions.

For more information about the Mortgage Forgiveness Debt Relief Act of 2007, see IRS Publication 4681: Canceled Debts, Foreclosures, Repossessions and Abandonments.

By Stephen Fishman Inman News *Disclaimer: For reference only. Everyone's situation is unique, please consult your CPA or attorney for your situation.

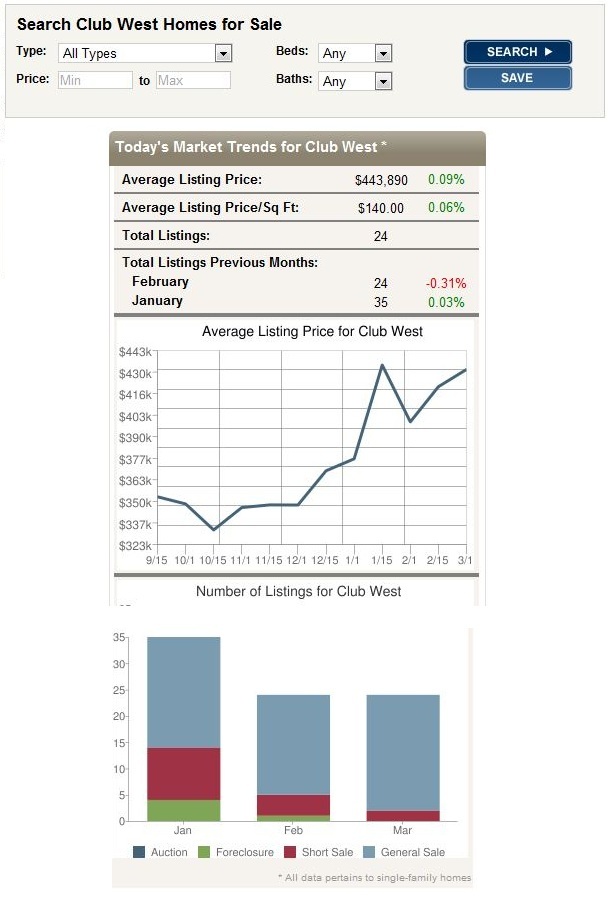

Welcome to the Club West homes and real estate portal: your single stop for finding a home in Club West. Here you can search every available home for sale in Club West.

As of today there are many homes and properties for sale that are available to search. The number of homes changes daily, so be sure to keep coming back right here, to the best site for Club West homes for sale.

Whether saving money or saving the planet is the motivation, there are thousands of simple "green" choices we can each make in our lives, and our homes, that will provide for a healthier, wealthier, more sustainable future.

Here are some quick tips to help you conserve water, energy (and money) in your home!*

If you don't have it in your budget to upgrade to a low-flow or dual–flush toilet, put a brick or full 2-liter bottle in your toilet tank. These will take up volume and help you save water every time you flush!

Turn down the temperature on your hot-water heater by at least 2 degrees and wrap your unit in a blanket.

Replace your burned-out incandescent light bulbs with CFLs or LEDs. Simply swapping out the most commonly used incandescent bulbs in your home can save you $60 to $100 a year.

Call me (480)-721-6253 if you're interested in learning more efficiency-boosting changes for your home!

And as always, when you or someone you know is interested in buying or selling real estate, I'm here to help!

*Information from the pages of A Keller Williams Realty Guide: Green Your Home.

Dobson Ranch Homes for Sale

Welcome to the Dobson Ranch homes and real estate portal: your single stop for finding a home in Dobson Ranch. Here you can search every available home for sale in Dobson Ranch.

As of today there are many homes and properties for sale that are available to search. The number of homes changes daily, so be sure to keep coming back right here, to the best site for Dobson Ranch homes for sale.

Do you owe more on the home then what its worth?

Are you or anyone you know UPSIDE down?

HARP 2.0 can help. NO APPRAISAL needed.

Not everyone can qualify for this program.

Call me for details. 480-721-6253.

In a move to increase their financial standing (and to get the FHA back into required capital requirements), on Monday, HUD announced their anticipated increases in the premiums they charge borrowers. Simply stated, the cost of borrowing is going up.

FHA loans, by design, are more liberal in their underwriting guidelines than most conventional loan products (in terms of credit, income ratios, required investment from the borrower, and maximum loan amount). HUD is not a lender. Rather, it is a federally-insured insurance company. They insure lenders against default on loans underwritten in compliance with their published guidelines. It is because of this insurance that lenders approve and close loans with more liberal guidelines.

As an insurance company, HUD charges two types of premiums on the FHA mortgages:

The UFMIP (Up Front Mortgage Insurance Premium) will be raised effective April 1, 2012 from its current 1% to 1.75%. One advantage to the UFMIP is the fact that it is typically built into the loan amount and does not require additional cash outlay at closing. However, the increase in loan amount does impact monthly payment and cash flow.

The MMIP (Monthly Mortgage Insurance Premium) will be raised 10 basis points on April 1, 2012 to cover the requirements of the payroll tax extension approved last year. This is a direct increase of 10 basis points in the borrower’s mortgage payment, and has the effect of a 10 basis point increase in interest rates. As a kicker, loans over $625,000 will be bumped 35 basis points from today’s levels effective June 1, 2012. This bump is substantial, as you can see in the chart below.

All information provided is deemed reliable but is not guaranteed and should be independently verified.

Swee Ng is a participant in affiliate advertising program designed to provide a means for sites to earn advertising fees. Swee has affiliate relationships with other companies, people and brands and when you click a link, he and his companies may receive a direct benefit.

1:54 PM

1:54 PM

Swee Ng

Swee Ng